New to High-Deductible Health Plan (HDHP)

Coverage through Anthem · Paired with a Health Savings Account (HSA)

The Heritage Group offers two High-Deductible Health Plan (HDHP) options for comprehensive medical and pharmacy coverage through Anthem. This page explains how HDHPs work so you can make a confident decision during enrollment.

For premium costs and plan documents, visit Health Plans page.

For enrollment steps, visit Benefits Enrollment page.

What is an HDHP?

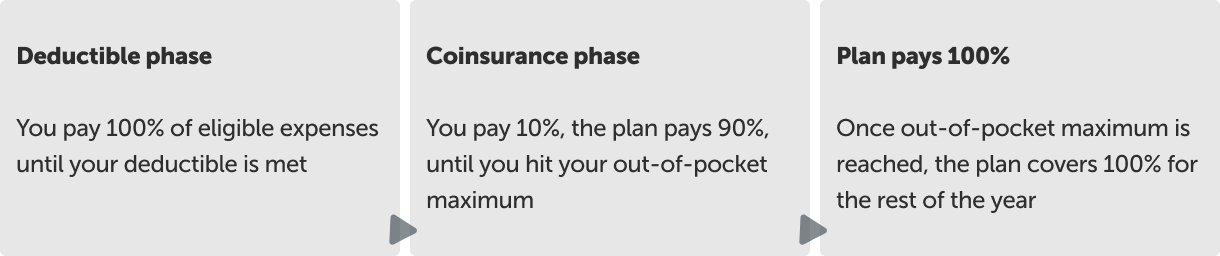

An HDHP is a health insurance plan with lower monthly premiums and a higher deductible than traditional health plans. You pay out-of-pocket for care until you meet your deductible. Once your deductible is met, you pay 10% coinsurance for covered services until your out-of-pocket maximum is reached. If you reach your out-of-pocket maximum, the plan will pay 100% for covered services for the remainder of the plan year.

Learn more about embedded out-of-pocket maximums for families below.

There is no copay for an in-network doctor’s office visit. The cost of the visit is applied to your medical deductible or coinsurance.

Eligible preventive care services and preventive prescription drugs are covered at 100%, meaning you pay nothing out of pocket for them.

| Feature | Option 1 | Option 2 |

| Deductible (Individual) | $2,000 | $4,000 |

|---|---|---|

| Deductible (Family) | $4,000 | $8,000 |

| Coinsurance (In-Network) | 10% | 10% |

| Out-of-Pocket Max (Individual) | $3,000 | $5,000 |

| Out-of-Pocket Max (Family) | $5,500 | $10,000 |

If you are an Individual covering only yourself, you are responsible for the first $2,000 (Option 1) or $4,000 (Option 2) in eligible expenses each year (the deductible).

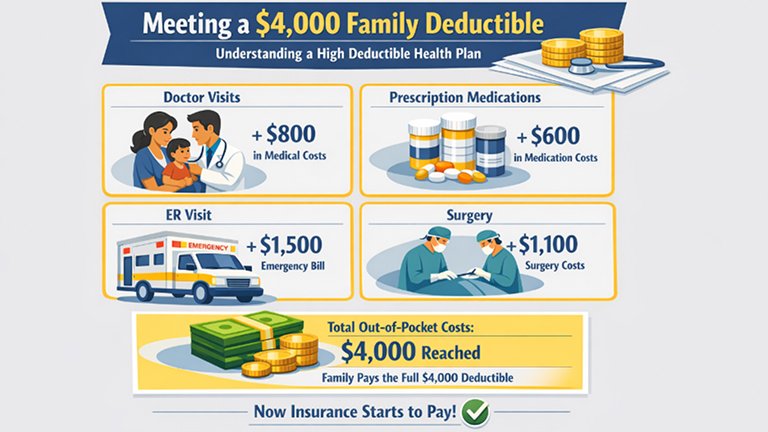

If you are covering your spouse, domestic partner, and/or child(ren), your family is responsible for the first $4,000 (Option 1) or $8,000 (Option 2) in eligible expenses. Each family members’ claims are applied to the Family deductible and accumulate toward the Family deductible.

Here is an example of a family meeting the Option 1 $4,000 deductible:

After the deductible is met, you enter the coinsurance (10%) phase and remain there until you reach the out-of-pocket (OOP) maximum. During the coinsurance phase, you are responsible for 10% of eligible expenses while the insurance plan pays 90%.

Plan pays 100%

When an Individual reaches the OOP maximum of $3,000 (Option 1) or $5,000 (Option 2), or a Family reaches the OOP maximum of $5,500 (Option 1) or $10,000 (Option 2), the insurance plan will begin paying 100% of eligible expenses for the remainder of the plan year.

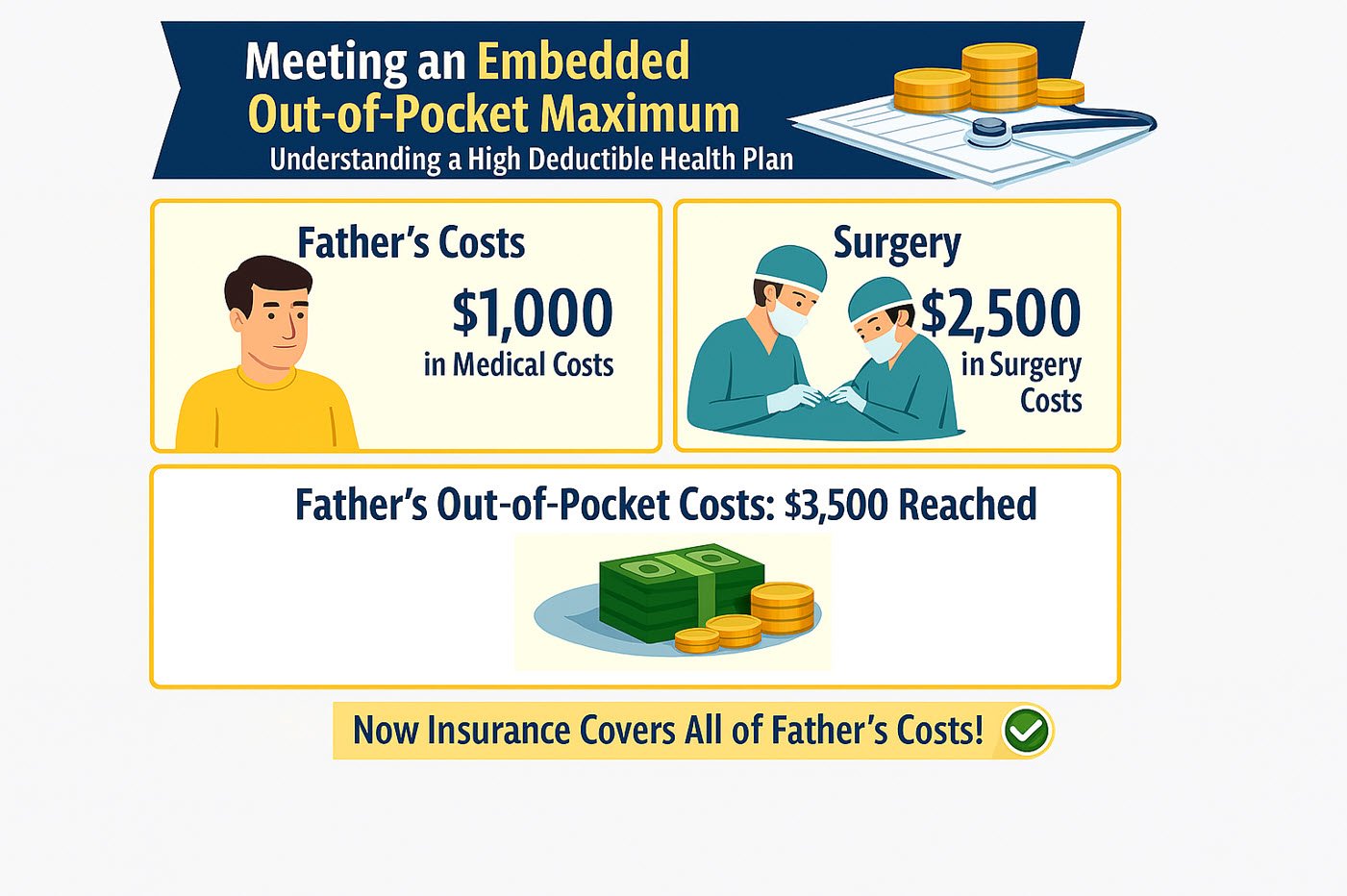

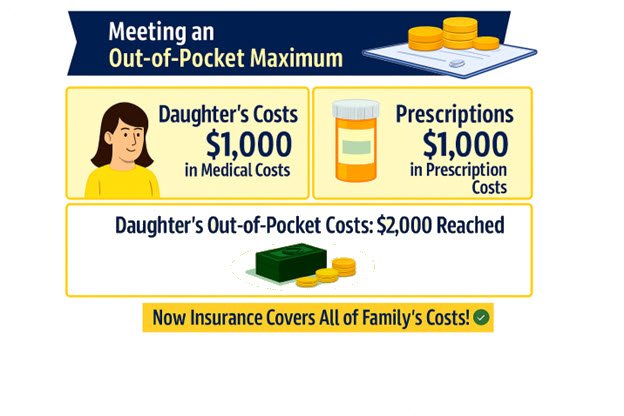

An embedded OOP maximum is the maximum amount one family member will pay for their covered services in a plan year. The embedded OOP amounts are $3,500 (Option 1) and $5,000 (Option 2).

If a family member meets the embedded OOP maximum, that member’s eligible expenses are paid at 100% for the remainder of the plan year, while the other family members’ eligible expenses continue to apply to the Family OOP maximum until it is reached.

Here is an example of the father of a family meeting the Option 1 $3,500 embedded OOP max:

Because the father’s eligible expenses met the embedded OOP maximum of $3,500, insurance covers 100% of his eligible expenses for the remainder of the plan year. His family members are still responsible for the remaining $2,000 toward the $5,500 Family OOP maximum. When one or more of his family members have paid the additional $2,000 in eligible expenses, the Family OOP maximum is met, and insurance covers 100% of the family’s eligible expenses for the remainder of the plan year.

Here is an example of the daughter of the family meeting the remaining $2,000 of the Option 1 $5,500 Family OOP maximum after the father met the embedded OOP maximum of $3,500:

• Basic search as a guest

• Select medical (includes pharmacy), dental, or vision

• Select IN

• Select Medical (Employer-sponsored)/Dental/Vision

• Select plan or network

- Medical - Blue Access PPO

- Dental - Dental Complete

- Vision - Blue View Vision

• Search based on type of provider, etc.

Prescription drugs fall into tiers, including generic, preferred brand, non-preferred brand, and specialty. Your cost at an in-network pharmacy or home delivery is 10% coinsurance after the deductible is met and until the OOP max is met.

Click here to review the list of free prescription drugs covered under our plans. The list is subject to change, so be sure to check it periodically.

You can choose how much you would like to contribute to your HSA on a pre-tax basis through payroll deductions. The money will be deposited into your Empower HSA, which is maintained by Optum and is yours to keep.

The company will also make contributions to your HSA on your behalf. The contribution amounts are based on your benefit effective date and coverage tier.

Why contribute to an HSA?

• Pre‑tax savings

• Unused funds roll over every year

• Portable — you keep it even if you leave the company

For contribution limits, investment options, and FSA details, visit the HSA & FSA page.

Please note that this discussion is for informational purposes only and is based on current regulations. It doesn’t represent and shouldn’t be construed as a substitute for professional advice. Please consult your personal legal, financial or tax counsel to discuss your personal situation.

Related pages

Resources

Ready to enroll?

For premium costs and plan documents, visit Health Plans page.

For enrollment steps, visit Benefits Enrollment page.

Need Help? Reach out to Employee Hub

Phone: 1-800-303-0408 | Email: [email protected]

* This portal only summarizes your benefit plans. If there is a discrepancy between the information on the portal and your carrier plan, the carrier plan will always govern.